Page 27 - Microsoft PowerPoint - TBS ACC - IFRS9 - Hedge Accounting - 20181126

P. 27

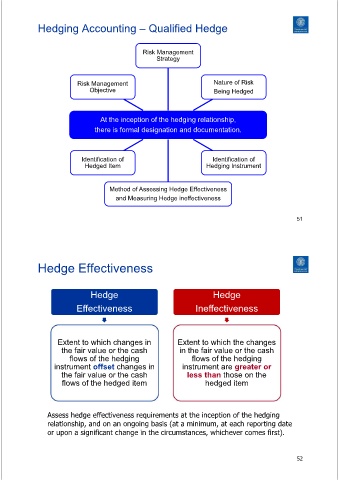

Hedging Accounting – Qualified Hedge

Risk Management

Strategy

Risk Management Nature of Risk

Objective Being Hedged

At the inception of the hedging relationship,

there is formal designation and documentation.

Identification of Identification of

Hedged Item Hedging Instrument

Method of Assessing Hedge Effectiveness

and Measuring Hedge ineffectiveness

51

Hedge Effectiveness

Hedge Hedge

Effectiveness Ineffectiveness

Extent to which changes in Extent to which the changes

the fair value or the cash in the fair value or the cash

flows of the hedging flows of the hedging

instrument offset changes in instrument are greater or

the fair value or the cash less than those on the

flows of the hedged item hedged item

Assess hedge effectiveness requirements at the inception of the hedging

relationship, and on an ongoing basis (at a minimum, at each reporting date

or upon a significant change in the circumstances, whichever comes first).

52